The Disability Tax Credit Resource Guide (Updated February 2026)

NOTE: Big news! The Ultimate 2026 Disability Tax Credit (DTC) Resource Guide is here—your go-to resource for the latest CRA regulations on applying, eligibility, Form T2201, and claiming your Disability Tax Credit.

Whether you’re filing for the first time or aiming to strengthen an existing claim, navigating Canada’s Disability Tax Credit may feel complex and overwhelming. This federal program helps individuals with severe and prolonged impairments, as well as those supporting them, reduce their income tax burdens and access related benefits. Officially defined by the Canada Revenue Agency (CRA), the Disability Tax Credit requires proof of marked functional limitations and a completed medical certification on Form T2201 before eligibility can be confirmed.

Today’s economic climate makes understand the DTC more important than ever. Inflation and high living costs continue to pressure households, while uneven job markets and trade tensions have slowed growth in several sectors. Many Canadians are feeling affordability strain across essentials like housing, healthcare, and transportation.

That reality makes knowing your disability tax entitlements essential. This updated 2026 guide reflects recent CRA updates, revised credit amounts, clear eligibility criteria, and improved application insights from the past year, with direct links to official CRA resources so you can verify details and claim with confidence.

Disability Tax Credit Guide – Key Takeaways (2026)

Our Disability Tax Credit Guide explains:

- Who may qualify for the Disability Tax Credit (DTC), including marked restrictions, cumulative effects, and life-sustaining therapy.

- How common diagnoses such as arthritis, diabetes, depression, autism, ADHD, chronic pain, and neurological conditions may relate to eligibility when they cause severe and prolonged functional limitations.

- The core CRA eligibility thresholds (3x longer, 90% of the time, and 12 months or more).

- Which impairment categories CRA recognizes and how they are assessed.

- How to complete and submit Form T2201, including who can certify each section.

- What to expect after submitting (review timelines, questionnaires, approvals, and denials).

- Common reasons applications are denied and how to strengthen a claim.

- How to claim the DTC after approval, including transferring the credit to a supporting person.

- How the DTC is calculated in 2026, including updated federal amounts and child supplements.

- How DTC approval can unlock related programs such as the RDSP, Child Disability Benefit, and Canada Disability Benefit.

Using accurate information and avoiding common mistakes can improve your chances of approval and help you claim the full tax credit available to you.

What Is the Disability Tax Credit (DTC)?

Quick Summary: What Is the Disability Tax Credit (DTC)?

- The Disability Tax Credit (DTC) is a federal tax credit for Canadians with severe and prolonged impairments

- The Disability Tax Credit can reduce income tax owed, but it is not a monthly payment.

- Approval requires Form T2201 and medical certification.

- CRA decides eligibility based on how your impairment affects daily functioning, not diagnosis alone.

- DTC approval may also help you access other disability-related programs (such as the RDSP and Canada Disability Benefit).

The Disability Tax Credit (DTC) is a federal income tax credit for Canadians with severe and prolonged impairments. Administered by the Canada Revenue Agency (CRA), it reduces income tax payable when an impairment causes ongoing limitations in daily functioning. Approval depends on medical certification and CRA review, not diagnosis alone.

The DTC is claimed through annual tax filings and is not a monthly payment. Because it is non-refundable, its value depends on whether the eligible person (or a supporting family member) had income tax payable during the approved years. CRA may also approve past years, allowing eligible individuals to claim the credit retroactively within reassessment limits.

DTC approval can also help unlock access to other disability-related programs and savings supports that require CRA confirmation. The credit includes both federal and provincial or territorial portions, and an additional child supplement may apply for individuals under 18.

How to Determine Your Eligibility for the Disability Tax Credit in 2026

Quick Summary: How to Determine DTC Eligibility in 2026

- CRA eligibility is based on limitations in daily activities such as walking, dressing, feeding, eliminating, hearing, speaking, vision, and mental functions.

- You do not qualify based on diagnosis alone.

- CRA looks at severity, how often the limitation occurs, and how long it has lasted.

- Updates made in 2022 expanded eligibility in key areas, including mental functions and life-sustaining therapy.

The Disability Tax Credit (DTC) applies to Canadians who live with severe and prolonged impairments, or with the cumulative effects of significant limitations. Many individuals search for answers based on a specific medical diagnosis. However, CRA does not approve applications based on a condition name alone. The key question is whether the condition results in a marked restriction, cumulative effect of significant limitations, or qualifying life-sustaining therapy.

According to the Canada Revenue Agency (CRA), eligibility depends largely on how an impairment affects a person’s ability to perform everyday functions, often described as activities of daily living. These functions include walking, dressing, feeding, eliminating, hearing, speaking, vision, and mental functions necessary for everyday life.

To qualify, it is important to understand that eligibility is not based on a diagnosis alone. A person may have a serious medical condition and still not qualify if daily functioning is not severely restricted. Conversely, a condition that may seem manageable on paper could qualify if it causes marked and prolonged limitations in everyday life.

CRA evaluates severity, duration, and functional impact, including whether limitations remain present all or almost all of the time. CRA’s eligibility framework was updated in 2022, expanding access in key areas, particularly mental functions necessary for everyday life and life-sustaining therapy. These updates clarified mental function criteria and adjusted how therapy time is calculated, including changes affecting individuals with Type 1 diabetes.

Get a free assessment

What Is the Disability Tax Credit Eligibility Criteria?

To be considered eligible for the Disability Tax Credit (DTC), you must:

- Be a Canadian citizen or a Permanent Resident of Canada.

- Have a medical practitioner certify that you have a severe and prolonged impairment or marked restriction in 1 of the categories.

- Have a medical practitioner certify that you have significant limitations in 2 or more categories.

- Or receive life-sustaining therapy to support vital function.

Eligible Disability Categories (CRA-Style Explanations)

Quick Summary: Eligible Disability Categories (CRA)

CRA eligibility is based on functional limitations, not diagnosis alone. In every category, CRA generally looks for the same core requirements:

- You are unable to perform the activity, or it takes at least 3 times longer than expected (even with treatment, medication, therapy, and assistive devices)

- The limitation is present all or almost all of the time (generally 90% or more)

- The limitation has lasted, or is expected to last, at least 12 months

Eligible Impairement categories include:

- Walking, mental functions, dressing, feeding, eliminating, hearing, speaking, and vision

- Cumulative effect of significant limitations (2+ categories)

- Life-sustaining therapy (requires ongoing medically necessary treatment)

A full category breakdown, including examples, is summarized in the chart below.

| CRA Category | What CRA Assesses | Common Examples | Who Can Certify Part B – T2201 |

| Walking | Ability to walk safely and effectively | Arthritis, MS, Parkinson’s, ALS, amputation | MD, NP, PT, OT |

| Mental Functions | Judgment, memory, regulation, adaptive functioning | Depression, anxiety, bipolar, autism, ADHD | MD, NP, Psychologist |

| Dressing | Putting on, fastening, removing clothing | Arthritis, Parkinson’s, MS | MD, NP, OT |

| Feeding | Preparing food, bringing to mouth, swallowing | Cerebral palsy, ALS, Parkinson’s | MD, NP, OT |

| Eliminating | Bowel or bladder control and management | Crohn’s, MS, spinal nerve damage | MD, NP |

| Hearing | Hearing and understanding speech | Deafness, severe hearing loss | MD, NP, Audiologist |

| Speaking | Verbal communication understood by others | Speech disorders, autism, ALS | MD, NP, Speech-language pathologist |

| Vision | Seeing well enough for daily tasks | Blindness, severe vision loss | MD, NP, Optometrist |

| Cumulative Effect | Combined impact of 2+ significant limitations | Chronic pain + fatigue, arthritis + depression | MD, NP |

| Life-Sustaining Therapy | Therapy supporting vital function (14+ hrs/week) | Type 1 diabetes, dialysis |

PLEASE NOTE: DTC approval does not automatically mean you will receive a refund or retroactive payment from the CRA. Approval simply confirms that the CRA considers your impairment eligible for the Disability Tax Credit. Because the DTC is a non-refundable tax credit, its value depends on whether you (or an eligible supporting family member) had income tax payable during the years you were approved. If no tax was owed in those years, there may be little or no tax reduction available, even if eligibility is granted.

Walking

The following impairments may be found eligible for the Disability Tax Credit’s walking category: arthritis, osteoarthritis, spinal stenosis, Parkinson’s disease, multiple sclerosis, cerebral palsy, amputation, ALS (amyotrophic lateral sclerosis), and gout. However, a diagnosis alone does not guarantee eligibility, since approval depends on how severely and consistently walking is restricted in daily life.

You must meet all 3 criteria below:

- You are unable to walk, or it takes you at least 3 times longer than someone of similar age without the impairment (even with appropriate therapy, medication, and devices)

- Your impairment is present all or almost all of the time (generally 90% or more)

- Your impairment has lasted, or is expected to last, for a continuous period of at least 12 months

Mental Functions (Mental Illness and Psychological Impairment)

To be considered under the Disability Tax Credit’s mental functions category, an individual must have a mental health condition or neurodevelopmental disorder such as depression, anxiety, bipolar disorder, autism spectrum disorder, ADHD, or a learning disability.

That said, the presence of a diagnosis on its own does not establish eligibility. The CRA looks beyond the label and assesses how markedly the condition restricts essential mental functions in everyday life, including memory, judgment, adaptive functioning, attention, problem-solving, emotional regulation, and goal-setting. Applicants must demonstrate how their impairment, such as ADHD, etc., substantially limits daily activities despite appropriate treatment, therapy, medication, or supports.

You must meet all 3 criteria below:

- You are unable to perform mental functions necessary for everyday life, or it takes you at least 3 times longer than someone of similar age without the impairment (even with appropriate therapy, medication, and supports)

- Your impairment is present all or almost all of the time (generally 90% or more)

- Your impairment has lasted, or is expected to last, for a continuous period of at least 12 months

Dressing

To be found eligible for the Disability Tax Credit under the dressing category, an applicant must show the CRA that their impairment results in a marked restriction in their ability to dress independently on a consistent basis.

Impairments that may fall under the Disability Tax Credit dressing category include arthritis, Parkinson’s disease, multiple sclerosis, cerebral palsy, spinal cord injuries, amputations, and intellectual or developmental disabilities.

Many individuals wonder whether having one of these conditions automatically qualifies them. It does not. The CRA does not approve claims based solely on a medical diagnosis. Instead, eligibility depends on how significantly the impairment limits the person’s ability to manage dressing in everyday life.

Dressing involves selecting appropriate clothing, putting garments on, fastening buttons or zippers, adjusting clothing as needed, and removing it safely. For some, these tasks remain substantially restricted even with treatment, therapy, or assistive devices.

Approval under this category is determined by functional limitation, not by the name of the condition.

You must meet all 3 criteria below:

- You are unable to dress yourself, or it takes you at least 3 times longer than someone of similar age without the impairment (even with appropriate therapy, medication, and devices)

- Your impairment is present all or almost all of the time (generally 90% or more)

- Your impairment has lasted, or is expected to last, for a continuous period of at least 12 months

Feeding

The following conditions may qualify under the Disability Tax Credit’s feeding category: cerebral palsy, ALS, Parkinson’s disease, and intellectual or developmental disabilities.

However, the presence of one of these conditions does not automatically result in approval. The CRA assesses how substantially the impairment limits a person’s ability to feed themselves in daily life.

Feeding includes preparing food for consumption, bringing food to the mouth, chewing, and swallowing safely. For some individuals, these basic activities remain markedly restricted on an ongoing basis, even with therapy, medication, or assistive devices.

Eligibility under this category is determined by the severity and persistence of functional limitations, not by diagnosis alone.

You must meet all three criteria below:

- You are unable to feed yourself, or it takes you at least 3 times longer than someone of similar age without the impairment (even with appropriate therapy, medication, and devices)

- Your impairment is present all or almost all of the time (generally 90% or more)

- Your impairment has lasted, or is expected to last, for a continuous period of at least 12 months

Eliminating (Bowel or Bladder Functions)

The following conditions may be considered under the Disability Tax Credit’s eliminating category: Crohn’s disease, ulcerative colitis, interstitial cystitis, multiple sclerosis, spinal nerve damage, and chronic incontinence.

Still, a medical diagnosis on its own does not confirm eligibility. The CRA reviews how significantly the impairment restricts a person’s ability to control and manage bowel or bladder functions safely and independently in everyday life.

Eliminating refers to bowel and bladder functions, including maintaining control, reaching a washroom in time, managing accidents, and handling necessary hygiene. For some individuals, these activities remain markedly limited on a continuous basis despite appropriate treatment, medication, or assistive devices.

Qualification depends on the extent and persistence of functional restriction rather than the name of the condition.

You must meet all 3 criteria below:

- You are unable to manage bowel or bladder functions, or it takes you at least 3 times longer than someone of similar age without the impairment (even with appropriate therapy, medication, and devices)

- Your impairment is present all or almost all of the time (generally 90% or more)

- Your impairment has lasted, or is expected to last, for a continuous period of at least 12 months

Hearing

The following impairments may fall under the Disability Tax Credit’s hearing category: hearing loss, deafness, and auditory processing disorder.

However, simply having one of these conditions does not automatically qualify an individual. The CRA examines how markedly the impairment limits a person’s ability to hear and understand spoken language in everyday environments, even when appropriate hearing aids, cochlear implants, or other assistive devices are in use.

Hearing, for DTC purposes, refers to the capacity to perceive and comprehend spoken communication in typical daily settings. Some individuals continue to experience severe and ongoing limitations despite properly fitted devices and treatment.

Eligibility in this category is determined by the degree of functional restriction present, not by the diagnostic label alone.

You must meet all 3 criteria below:

- You are unable to hear, or it takes you at least 3 times longer than someone of similar age without the impairment (even with appropriate devices, therapy, and treatment)

- Your impairment is present all or almost all of the time (generally 90% or more)

- Your impairment has lasted, or is expected to last, for a continuous period of at least 12 months

Speaking

The following conditions may be considered under the Disability Tax Credit’s speaking category: speech disorders, autism spectrum disorder, cerebral palsy, ALS, and other impairments that affect verbal communication.

That said, a diagnosis by itself does not establish eligibility. The CRA evaluates how significantly the impairment restricts an individual’s ability to communicate verbally in a manner that can be understood by others in everyday settings.

Speaking, for DTC purposes, refers to the capacity to express oneself clearly enough to be understood in typical daily environments. Some individuals remain markedly limited in this area despite therapy, assistive devices, or alternative communication supports.

Qualification under this category depends on the severity and persistence of functional limitations rather than the name of the condition.

You must meet all 3 criteria below:

- You are unable to speak, or it takes you at least 3 times longer than someone of similar age without the impairment (even with appropriate therapy, medication, and devices)

- Your impairment is present all or almost all of the time (generally 90% or more)

- Your impairment has lasted, or is expected to last, for a continuous period of at least 12 months

Vision

The following conditions can fall under the Disability Tax Credit’s vision category: legal blindness, advanced glaucoma, macular degeneration, profound vision loss, and other serious ocular disorders.

Still, eligibility does not hinge on the condition’s name. The CRA relies on objective visual measurements and real-world impact. They look at visual acuity, visual field, and how those limitations affect safe, independent functioning in daily environments, even after corrective lenses or medical intervention.

Vision, within this category, means more than having an eye diagnosis. It refers to whether a person can see well enough to navigate spaces, read essential information, recognize faces, or complete routine tasks without significant difficulty.

Approval depends on documented visual impairment that meets CRA thresholds and demonstrates sustained restriction in everyday life.

You must meet all 3 criteria below:

- You are unable to see, or it takes you at least 3 times longer than someone of similar age without the impairment (even with appropriate therapy, medication, and devices)

- Your impairment is present all or almost all of the time (generally 90% or more)

- Your impairment has lasted, or is expected to last, for a continuous period of at least 12 months

Cumulative Effect of Significant Limitations (Combine 2 or more categories)

Some individuals assume they do not qualify for the Disability Tax Credit because no single impairment leaves them markedly restricted on its own. In certain cases, however, several significant limitations can interact and together create a level of overall restriction comparable to a marked restriction in one category.

The cumulative effect category may apply to conditions such as chronic pain, fibromyalgia, arthritis, diabetes with complications, depression combined with physical impairments, or fatigue-related disorders. What matters is not the individual diagnoses, but how their combined impact substantially limits everyday functioning across multiple basic activities.

Under this provision, the CRA evaluates the total functional burden created by all impairments working together. Eligibility depends on the overall degree of restriction experienced in daily life, rather than on any single diagnosis considered in isolation.

You must meet all 3 criteria below:

- You have significant limitations in two or more categories, and the combined effects cause a level of restriction comparable to being markedly restricted in one category

- Your limitations are present all or almost all of the time (generally 90% or more)

- Your limitations have lasted, or are expected to last, for a continuous period of at least 12 months

Life-Sustaining Therapy

The Disability Tax Credit also includes a life-sustaining therapy category for individuals who must undergo ongoing treatment to support a vital bodily function. To qualify, the therapy must be medically necessary, required at least three times per week, and meet the CRA’s minimum weekly time threshold when eligible activities are properly calculated.

This provision commonly applies to individuals with Type 1 diabetes, as well as others who depend on intensive, continuous treatment to maintain health. The CRA applies detailed rules when calculating eligible time, which can make this category more technical than others.

Later in this guide, we outline how life-sustaining therapy is assessed, what activities may count toward the weekly requirement, and what medical documentation is generally needed to support an application.

What is “Prolonged Impairment” as it pertains to Eligibility for the Disability Tax Credit

The CRA has identified “prolonged impairment” as the working condition to determine one’s eligibility for the DTC.

The following is what they look for when determining if an impairment is considered prolonged:

- The individual requires and receives extensive therapy to aid in performing activities of daily living.

- The individual has had surgeries, hospitalizations, short and long-term disability, employment restrictions, etc.

- The individual’s impairment has lasted or is expected to last for a minimum of 12 consecutive months.

Prolonged Impairments Commonly Considered in DTC Eligibility

For Disability Tax Credit purposes, the Canada Revenue Agency evaluates whether an impairment is both severe and prolonged, meaning it has lasted, or is expected to last, at least 12 months and causes ongoing functional limitations. Eligibility is based on how an impairment affects daily functioning rather than the diagnosis name itself.

The following conditions are commonly associated with prolonged impairments that may meet DTC eligibility criteria when functional limitations are present and supported by medical certification:

This list is not exhaustive and does not guarantee eligibility. CRA assesses each application individually based on severity, duration, and functional impact, as documented by a qualified medical practitioner.

What Does “Markedly Restricted” Mean for DTC Eligibility?

CRA may consider you markedly restricted if, even with treatment, medication, and assistive devices:

- You cannot perform a basic daily activity independently, OR

- You can perform it, but it takes at least 3 times longer than someone your age without the impairment

To qualify, the restriction must also:

- Be present all or almost all of the time (generally 90% or more)

- Last, or be expected to last, at least 12 months

You may also qualify through the cumulative effect of significant limitations if 2 or more categories combine to create an overall restriction comparable to one marked restriction.

CRA uses the term “markedly restricted” to describe a severe limitation in a basic activity of daily living. A person may be considered markedly restricted when, even with appropriate therapy, medication, and assistive devices, one of the following applies:

- They are unable to perform the activity on their own

- They can perform the activity, but it takes an inordinate amount of time

“Inordinate amount of time” generally means the person takes at least three times longer than someone of similar age who does not have the impairment.

For DTC purposes, the restriction must be present all or almost all of the time, which CRA generally interprets as at least 90% of the time.

Marked restriction may also be supported through a cumulative effect of significant limitations. This applies when a person has two or more significant limitations that exist together all or almost all of the time and, when combined, create an overall impact comparable to being markedly restricted in one category.

Example

Greg was diagnosed with osteoarthritis and required knee surgery due to significant joint damage. Even after treatment, walking takes him at least three times longer than someone of similar age without the impairment. Dressing also takes substantially longer, since he must sit, move carefully, and take frequent breaks due to pain and stiffness. Because these restrictions remain present all or almost all of the time and have lasted continuously, his functional limitations may meet CRA’s markedly restricted criteria.

Eligibility for the Disability Tax Credit for Physical Impairments

Quick Summary: Physical Impairments and Diabetes (DTC)

- Physical impairments Eligibility is based on how the impairment affects daily functioning, not diagnosis alone.

- CRA looks for a severe and prolonged restriction in one or more eligible categories (such as mobility, vision, hearing, speech, feeding, dressing, or elimination).

- The limitation must meet CRA’s marked restriction or cumulative effect criteria.

Diabetes

- Diabetes does not qualify automatically.

- Most approvals are assessed under life-sustaining therapy rules.

- Type 1 diabetes may qualify if CRA’s weekly treatment time requirements are met.

- Type 2 diabetes usually does not qualify unless intensive insulin therapy or other severe functional limitations are present.

- Eligibility depends on medical necessity and whether CRA’s time threshold is met.

Many people ask whether they qualify for the Disability Tax Credit because they have a physical condition such as arthritis, spinal stenosis, Parkinson’s disease, multiple sclerosis, chronic pain, COPD, or another long-term medical diagnosis. A diagnosis alone does not determine eligibility. CRA evaluates how severely the condition affects daily functioning.

Physical impairments can affect many parts of daily functioning, including mobility, vision, hearing, speech, feeding, dressing, and bowel or bladder control. CRA assesses whether the impairment causes a severe and prolonged restriction in one or more eligible categories, even with appropriate therapy, medication, and devices.

Physical impairments commonly relate to limitations in areas such as chronic pain-related mobility issues, vision, hearing, elimination, respiratory endurance, and other functional restrictions that interfere with everyday tasks. However, eligibility depends on whether these limitations meet CRA’s marked restriction, cumulative effect, or life-sustaining therapy criteria.

Diabetes and DTC Eligibility (2026)

Diabetes does not qualify someone for the DTC based on diagnosis alone. CRA eligibility typically depends on whether the person meets the criteria under life-sustaining therapy, which focuses on both medical necessity and time spent on required treatment.

- Type 1 diabetes: Many individuals with Type 1 diabetes may qualify under life-sustaining therapy if CRA’s treatment time requirements are met. Approval is not automatic and still depends on meeting CRA’s criteria.

- Type 2 diabetes (not using intensive insulin therapy): Type 2 diabetes alone generally does not qualify under life-sustaining therapy unless other severe functional limitations are present in a different category.

- Type 2 diabetes (using intensive insulin therapy): Some individuals may qualify if they meet CRA’s life-sustaining therapy rules, including the required weekly time threshold.

- Insulin-dependent diabetes (not classified as Type 1): Eligibility depends on whether life-sustaining therapy criteria are met, including CRA’s time calculation rules.

This guide explains life-sustaining therapy in detail later, including how CRA counts treatment time and what documentation is typically required.

Eligibility for the Disability Tax Credit for Mental and Psychological Impairments

Quick Summary: Mental, Neurological, and Life-Sustaining Therapy

- CRA eligibility is based on functional impact, not diagnosis alone.

- Mental impairments may qualify when mental functions necessary for everyday life are severely and continuously restricted (such as memory, judgment, attention, and regulating behaviour).

- Neurological conditions may qualify if they cause severe, prolonged limitations in daily activities.

- Life-sustaining therapy may qualify when it supports a vital function, is medically necessary, is required at least twice weekly, and averages 14+ hours per week for at least 12 months.

Many people ask whether they qualify for the Disability Tax Credit because they have a condition such as depression, anxiety, bipolar disorder, PTSD, schizophrenia, or another mental health diagnosis. A diagnosis alone does not determine eligibility. CRA evaluates how severely the condition affects everyday functioning.

Mental illness and psychological impairments can significantly interfere with self-care, safety, judgment, memory, emotional regulation, and the ability to live independently.

Under CRA rules, you may qualify if your impairment causes a severe and prolonged restriction in mental functions necessary for everyday life. Eligibility depends on functional impact, not diagnosis, and limitations must be present all or almost all of the time and meet CRA’s marked restriction criteria.

CRA’s framework includes areas such as adaptive functioning, attention, concentration, judgment, memory, problem-solving, regulating behaviour and emotions, and verbal or non-verbal comprehension.

Eligibility for the Disability Tax Credit for Neurological Impairments

Neurological impairments affect the brain and prevent it from accurately or consistently controlling the body in severe cases. Working with a neurological impairment can be incredibly difficult as it makes things such as holding objects or walking independently challenging. CRA considers the following conditions as potentially eligible neurological impairments for the Disability Tax Credit:

- Multiple sclerosis

- Alzheimer’s disease

- Parkinson’s disease

- Epilepsy

- Stroke

Eligibility for the Disability Tax Credit for Impairments requiring Life-Sustaining Therapy

Life-sustaining therapy may qualify an individual for the Disability Tax Credit when the therapy supports a vital function and meets CRA’s time and frequency requirements. Eligibility is based on the medical necessity of the therapy and the amount of time required to administer it, not on diagnosis alone.

To meet CRA’s criteria, all of the following must apply:

- The therapy is required to support a vital function

- The therapy is needed at least two times per week

- The therapy requires an average of at least 14 hours per week, calculated over a representative period

- The requirement has lasted, or is expected to last, for a continuous period of at least 12 months

CRA considers only the time spent directly completing therapy-related activities when assessing the 14-hour requirement. This includes time taken away from regular daily activities to administer treatment, as well as time needed to set up and operate portable devices.

In certain situations, CRA also allows additional therapy-related time to be included. This may apply when a person must regularly adjust medication dosages as part of the therapy itself, where time spent determining and administering dosage counts toward the weekly total. It may also apply when therapy requires daily intake of a specialized formula or food to meet medical needs, and time must be spent calculating the appropriate amount. For children who are too young to perform therapy activities independently, the time another person spends administering and supervising the therapy may also count toward the weekly requirement.

Example

Louis requires ongoing therapy to support a vital function. His treatment involves multiple daily interventions and monitoring tasks that, when combined, require an average of at least 14 hours per week. Because this therapy is medically necessary, occurs at least two times per week, and meets CRA’s time requirement on an ongoing basis, it may meet the criteria for life-sustaining therapy under the Disability Tax Credit.

Claiming the Disability Tax Credit

Quick Summary: Claiming the Disability Tax Credit

- DTC approval does not automatically create a payment. The credit must be claimed on an income tax return.

- The DTC is non-refundable, it only reduces income tax owed.

- The eligible individual can claim the credit, or transfer unused amounts to a supporting person.

- Transfers are most common to a spouse/common-law partner, parent, grandparent, or other eligible family member.

- CRA may allow retroactive adjustments for approved past years, and the credit can also be claimed each year going forward.

- If the eligible person has low or no taxable income, the credit may still be valuable when transferred to a supporter or when child-related benefits apply.

Once the Canada Revenue Agency (CRA) approves a Disability Tax Credit (DTC) application, the credit must still be claimed on an income tax return. Because the DTC is a non-refundable tax credit, its value depends on whether the eligible person, or someone supporting them, had income tax payable during the approved years.

Get a free assessment

Who Can Claim the DTC?

A person may be both the eligible individual and the claimant. In other situations, the eligible individual may not have enough taxable income to benefit from the credit, and an eligible supporting person may claim all or part of the amount instead.

The Eligible Individual

The eligible individual is the person whose impairment has been approved by CRA under DTC eligibility rules. This person may claim the disability amount on their own return if they have enough income tax payable to use the credit.

In many cases, an eligible individual may have low or no taxable income due to reduced work capacity. When this happens, unused portions of the credit may be transferred to a supporting person who qualifies under CRA rules.

The Claimant

A claimant is the person who claims the disability amount on their tax return, either for themselves or as a supporting person claiming an unused portion.

CRA generally allows a transfer when the eligible individual depends on the claimant for support. In most cases, the claimant must be related to the eligible individual as a spouse or common-law partner, parent, grandparent, child, grandchild, sibling, aunt, uncle, niece, or nephew.

In some situations, a person who is not related may still qualify if they can demonstrate that they provided support for basic necessities of life such as food, shelter, and clothing.

To learn more, CRA provides guidance under Line 31800 – Disability amount transferred from a dependent.

Note: If you did not pay child support for a child, you generally cannot claim the transferred disability amount for that child. If you were separated from a spouse or common-law partner for part of the year, special CRA rules may apply.

Transferring the Credit

If the eligible individual does not need the full disability amount to reduce their own income tax payable, CRA may allow the unused portion to be transferred to a supporting person.

Transfers are most commonly claimed by:

- a spouse or common-law partner

- a parent or grandparent

- another eligible family member who provides support

CRA evaluates transfers based on relationship, support provided, and whether the eligible individual used any portion of the credit themselves.

Transferring the disability amount is done through the tax return. CRA’s rules and line references vary depending on the relationship and the type of dependent.

For full CRA guidance on claiming and transferring the DTC, refer to the CRA page: Claiming the Disability Tax Credit.

In some situations, the unused portion of the disability amount may be split between more than one supporting person. The total amount claimed by all supporters combined cannot exceed the maximum disability amount allowed for that dependent.

Eligibility for the Disability Tax Credit is not based on income or taxes paid. Paying federal income tax is not a requirement to qualify for the DTC. Once eligibility is confirmed, unused credits may be transferred to an eligible supporting person for some or all approved years.

In cases involving a child approved for the Disability Tax Credit, the child does not need to have taxable income. When a child is found eligible, DTC approval may result in an increase to the Canada Child Benefit for the approved years, depending on family circumstances.

How the DTC Is Paid Out

The Disability Tax Credit does not function as a monthly payment. It is claimed through income tax filings and can reduce income tax payable for the years CRA approves.

In general, the DTC may apply in two main ways:

- Retroactive tax adjustments: CRA may approve eligibility for past years, and the disability amount may be applied to those years through tax return adjustments. If income tax was payable in those years, this may result in a refund.

- Ongoing annual claiming: Once approved, the disability amount can be claimed each year on the eligible person’s tax return, or transferred to a supporting person if applicable, for as long as CRA approval remains valid.

Some approvals are granted for limited periods. When the approval end date is reached, CRA may require a new application or updated medical certification to continue claiming the credit.

Note: In some cases, the CRA may send a letter asking for additional information to confirm who is claiming the credit. The letter will contain a reference number and instructions on what to do.

How to Apply For Disability Tax Credit

Quick Summary: How to Apply for the Disability Tax Credit

- To apply, you must submit Form T2201 (Disability Tax Credit Certificate) with medical certification.

- You can complete the application digitally or using the PDF version.

- Part A is completed by the applicant (or representative). Part B must be completed by an authorized medical practitioner.

- You can apply: On your own, With help from an accountant or bookkeeper, and With help from a Disability Tax Credit firm.

- Many applications are denied due to incomplete or unclear medical explanations, even when eligibility exists.

There are two ways to complete Form T2201 (Disability Tax Credit Certificate): a digital application through CRA, or a manual PDF version. In both cases, Part A must be completed by the applicant (or representative), and Part B must be completed and certified by an authorized medical practitioner.

Although the application process may seem straightforward, many Canadians are denied each year due to incomplete forms, unclear medical explanations, or missing functional details.

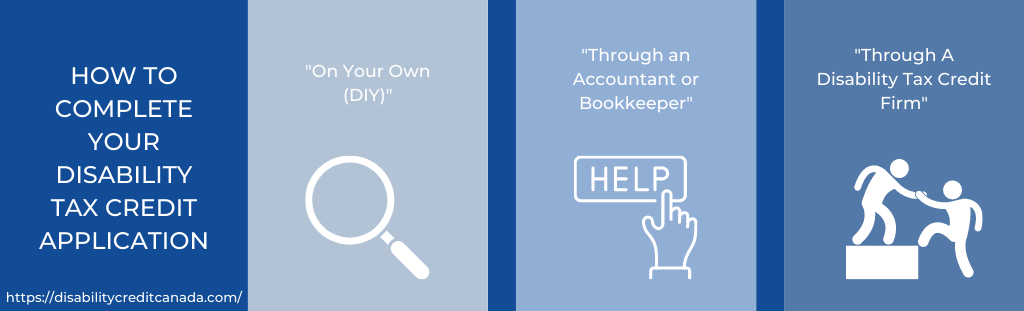

Below are the three most common ways people apply for the Disability Tax Credit.

Option 1: Apply on Your Own (DIY)

This option is best for applicants whose impairments are clearly documented and whose medical practitioner understands CRA’s eligibility requirements.

To apply on your own:

- Complete Part A of Form T2201

- Have your medical practitioner complete Part B

- Submit the form to CRA online or by mail

The main cost is typically the medical practitioner’s fee for completing Part B. In many cases, this fee may be claimed as a medical expense on your tax return.

Option 2: Apply With an Accountant or Bookkeeper

Some applicants choose to apply with the help of an accountant or bookkeeper, especially if they already have someone preparing their taxes.

However, most accountants do not provide medical guidance and will still rely on your medical practitioner to describe how your impairment affects daily functioning under CRA rules.

Option 3: Apply With a Disability Tax Credit Firm

Some Canadians choose to work with a specialized Disability Tax Credit firm, such as Disability Credit Canada, to help with the application process.

A specialized firm may help by:

- reviewing medical records and identifying eligible categories

- coordinating with your medical practitioner to improve functional descriptions

- assisting with CRA follow-up questionnaires

- applying for eligible retroactive tax adjustments and related programs after approval

Many firms operate on a no-win, no-fee basis. If approved, the firm typically charges a percentage of the retroactive tax credits or refunds obtained.

Challenges of Getting Approved for the Disability Tax Credit

Quick Summary: Common Challenges (and What to Do)

- Many DTC applications are denied due to unclear medical wording or incomplete functional details.

- A doctor may be unsupportive, rushed, or unfamiliar with CRA eligibility rules.

- CRA criteria can be strict and difficult to interpret without guidance.

- Some approvals expire and require reapplication, even when the impairment continues.

- CRA feedback is often limited, which can make it hard to understand why an application was denied.

There are several challenges involved with getting approved for the DTC. In this section, we will go over each in detail, and we’ll explain what you can do about it.

- Unsupportive doctor: When we refer to an unsupportive doctor, it may indicate two scenarios: either your doctor comprehends the eligibility criteria but believes you do not qualify for the program, or your doctor lacks understanding of the Disability Tax Credit’s eligibility requirements, thus deeming you ineligible.

- Complex rules: The complexity of the rules implies the intricate nature of the eligibility criteria set by the Canada Revenue Agency (CRA), which can be challenging to navigate for applicants and healthcare professionals alike.

- Stringent criteria: Stringent criteria highlight the rigorous standards set by the CRA for determining eligibility, necessitating substantial evidence and documentation to prove qualification for the Disability Tax Credit.

- Reapplication requirements: Reapplication requirements signify the need for previously approved applicants to undergo the application process again after a certain period, irrespective of the severity or permanence of their disability.

- Lack of clarity in the application process: The lack of clarity in the application process points to the absence of clear guidelines or consistent feedback from the CRA, leading to confusion and uncertainty among applicants regarding the necessary steps and requirements.

Some Tips to Get Around-

- Unsupportive doctor: If faced with an unsupportive doctor, consider presenting them with the eligibility requirements. Alternatively, seek a second opinion from another healthcare provider who may have a different perspective on your eligibility for the Disability Tax Credit.

- Complex rules: To navigate the complexity of the rules, consider consulting with a tax professional or disability advocate who can provide guidance and assistance in understanding and fulfilling the eligibility criteria.

- Stringent criteria: When confronted with stringent criteria, ensure that you gather comprehensive documentation and evidence to support your application, and consider seeking assistance from healthcare providers experienced in completing DTC forms.

- Reapplication requirements: In response to reapplication requirements, familiarize yourself with the renewal process and ensure timely submission of necessary documentation to maintain eligibility for the Disability Tax Credit.

- Lack of clarity in the application process: To address the lack of clarity in the application process, reach out to the Canada Revenue Agency (CRA) for clarification on specific requirements and seek assistance from disability advocacy organizations or legal professionals if needed.

How to Fill – Disability tax credit form/certificate T2201 (DTC)

Form T2201, Disability Tax Credit Certificate consists of 2 main parts:

T2201-Part A

Under the “Individual’s section,” of Form T2201, the CRA requires you to provide personal information for the disabled person and/or claimant. Some of the information you will be asked to provide is as follows: Name, Address, Date of Birth, and Social Insurance Number. Additionally, if you want to adjust your tax returns make sure that is indicated in question 3 of Part A.

T2201-Part B

Under the “Medical practitioner’s section” of Form T2201, your medical practitioner will be asked to fill out and certify the information provided in the sections that apply is correct and complete, then sign the form.

- In this section the correct medical practitioner will be asked to certify your medical impairment resulting from a condition and the effects of said impairment on your activities of daily living in several areas, such as Vision, Speaking, Hearing, Walking, Eliminating, Feeding, Dressing, Mental functions, Cumulative effect of significant limitations, & Life-sustaining therapy.

- The corresponding health care practitioner must initial beside their designation and fill out each of the impairment sections that apply to you.

- Cumulative Effect of Significant Limitation, Page 14: This page of Form T2201, is only applicable to those persons who experience limitations in more than one impairment category, concerning the cumulative effects of their daily living restrictions.

- Life-Sustaining Therapy, Page 15: This page is only applicable to those persons who are using life-sustaining therapy.

Who Can Fill Out Part B of Form T2201?

Part B of Form T2201, Disability Tax Credit Certificate must be completed and certified by an approved medical practitioner. CRA only accepts certification from specific practitioner types, depending on the impairment category being claimed.

Below is a list of medical practitioners authorized to certify Part B of Form T2201:

| Authorized Medical Practitioner | Impairment Category |

| Medical doctor | All impairments |

| Nurse practitioner | All impairments |

| Optometrist | Vision |

| Audiologist | Hearing |

| Occupational therapist |

|

| Psychologist | Mental functions necessary for everyday life |

| Speech-language pathologist | Speaking |

If your medical practitioner charges a fee for completing the DTC application, you are responsible for paying it. However, you may be able to claim this fee as a medical expense on your tax return, depending on your tax situation and CRA rules.

How to Submit Form T2201, Disability Tax Credit Certificate

Quick Summary: CRA Review, Approval, or Denial

- After submitting Form T2201, CRA review typically takes 3–6 months.

- CRA may approve, deny, or request additional medical information.

- If approved, you will receive a Notice of Determination confirming eligible years.

- If denied, the notice will explain the reason.

- You can check your application status through My CRA Account.

- If you disagree with the decision, you may request a review, submit updated medical information, or file a formal objection within 90 days.

Once Form T2201 has been completed and certified by your medical practitioner, it must be submitted to the Canada Revenue Agency along with any required supporting documentation. This can be done in one of the following ways:

- Electronically, using the “Submit documents” feature in My CRA Account or through Represent a Client

- By mail to your nearest CRA tax centre

It is important to keep a copy of the completed form and any attachments for your records.

After submitting Form T2201, CRA’s review process typically takes between three and six months. During this period, one of the following outcomes may occur:

- If CRA requires more information, they may send a questionnaire directly to the medical practitioner who completed Part B. The practitioner must respond and return the requested information within the specified timeframe.

- CRA may approve the application. If approved, CRA will issue a Notice of Determination outlining the years you were found eligible for the Disability Tax Credit. CRA may also reassess prior tax years and issue any applicable refunds.

- CRA may deny the application due to insufficient information, contradictory details, or ineligibility under DTC criteria.

Checking the Status of Your DTC Application

You can check the status of your Disability Tax Credit application through your CRA account. The progress tracker in My CRA Account allows you to view updates and see where your application is in the review process.

How Long Does it Take to Process a Disability Tax Credit Application?

Regardless of the method used to complete your Disability Tax Credit Application, it will typically take between 3 to 6 months for the CRA to assess the application and determine if you’re eligible for the Disability Tax Credit (DTC). However, this time frame can vary depending on the time of year, processing centre location, and the complexity of your impairment or application.

Furthermore, if your application is approved for previous years, your tax returns will have to be reassessed. As such, it may take 1-3 months or so to process your retroactive tax credits. On average, it will usually take 3 months to process a new application, but some can take up to a year before they are finalized.

NOTE: To quickly find out when you can expect the CRA to complete your request or get back to you about the status of your application, you can use the Check CRA Processing Times tool for further assistance.

CRA’s Decision About Your DTC Application

Once the Canada Revenue Agency completes its review of Form T2201, you will receive a written decision by mail called a Notice of Determination. This notice confirms whether CRA approved or denied the application and outlines what happens next.

If CRA Approves Your Application

When an application is approved, CRA will confirm the specific year or years you qualify for the Disability Tax Credit. After that, the DTC can be claimed on an income tax return for the approved years.

In most cases, you do not need to submit a new application every year. Re-application only becomes necessary if CRA requests updated information or sets an end date on the approval period.

If CRA Denies Your Application

If CRA denies the application, the Notice of Determination will include the reason for the denial. CRA decisions are generally based on the medical practitioner’s answers and functional descriptions provided in Part B of Form T2201.

If a denial occurs, one practical step involves reviewing your submitted T2201 and comparing it with CRA’s stated reasons. Many denials result from missing details, unclear functional explanations, or information that does not match CRA’s eligibility thresholds.

If You Disagree With CRA’s Decision

If you believe CRA’s decision does not reflect your functional limitations, several options may be available depending on the situation:

You may contact CRA for clarification on the decision.

You may request a review and submit new or updated medical information from a practitioner familiar with your limitations.

You may submit a new T2201 with stronger functional explanations or additional supporting documentation.

You may also file a formal objection. In most cases, objections must be filed within 90 days of the date shown on the Notice of Determination.

For CRA’s official guidance on Notices of Determination, review outcomes, and next steps after approval or denial, refer to CRA’s page: Review the decision on your Disability Tax Credit application.

Appealing a Denial of Your Disability Tax Credit Application

If CRA denies your DTC application, the Notice of Determination will explain why. CRA’s decision is based on the information provided by the medical practitioner on Form T2201.

Filing a Formal Objection (Notice of Objection)

You can file a Notice of Objection in three ways:

- Online: Log into My Account for Individuals or My Business Account and select “Register my formal dispute” (Notice of Objection). You will receive a case number. Supporting documents can be uploaded using “Submit documents online.”

- Through a representative: An authorized representative can file using Represent a Client and selecting “Register my formal dispute.”

- By mail or fax: Submit Form T400A, Objection – Income Tax Act, or a signed letter explaining your reasons.

Send it to:

Chief of Appeals

Appeals Intake Centre

1050 Notre Dame Avenue

Sudbury ON

P3A 5C1

For full details, refer to CRA’s official guidance on filing a Notice of Objection.

Common Reasons For DTC Denial

- Incomplete form: Missing or unclear information on Form T2201 is a common reason for denial. Review the form carefully before submitting.

- Medical practitioner issues: Some doctors may be unfamiliar with DTC rules or may not fully explain your limitations. Choose a practitioner who understands the criteria and is willing to provide detailed information.

- Lack of knowledge: Not all medical professionals understand how CRA assesses eligibility.

- Inconsistent information: If details on the form do not match follow-up responses, CRA may deny the application.

- Impairment focus: CRA evaluates how your condition affects daily activities, not the diagnosis itself.

- Duration requirement: The impairment must last at least 12 months and affect you 90% or more of the time.

- Cumulative effects: If multiple limitations combine to create a severe impact, this should be clearly documented.

- Supporting documents: Include relevant medical records or reports that support your claim.

How is the Disability Tax Credit Calculated?

Quick Summary: How the Disability Tax Credit Is Calculated

- The DTC includes a federal amount and a provincial or territorial amount.

- It consists of a Base Amount, and for eligible children under 18, a Supplemental Amount.

- For 2025, the federal disability amount is $10,341.

- The 2025 child supplement maximum is $6,032.

- The federal credit equals 14.5% of the disability amount.

- The provincial portion is roughly 10%, depending on the province.

Understanding how the Disability Tax Credit (DTC) is calculated can be confusing, especially because the credit amount depends on tax payable and varies by province. In general, the DTC includes a federal and provincial portion, made up of a Base Amount and, for eligible individuals under 18, a Supplemental Amount.

For province-specific base and supplement tables for the past 10 years, refer to our provincial DTC guides.

- Alberta Disability Tax Credit Application

- British Columbia Disability Tax Credit Application

- Ontario Disability Tax Credit Application

- Nova Scotia Disability Tax Credit Application

- Saskatchewan Disability Tax Credit Application

- Newfoundland and Labrador Disability Tax Credit Application

- Quebec Disability Tax Credit Application

- Manitoba Disability Tax Credit Application

- New Brunswick Disability Tax Credit Application

The “Base Amount” and “Supplemental Amount” portions are provided by both federal and provincial sources, as follows:

- The federal DTC portion is 14.5% of the disability amount for that tax year.

- The “Base Amount” maximum for 2025 is $10,341, according to the Canada Revenue Agency’s (CRA’s) indexation chart.

- The “Supplemental Amount” for children with disabilities for 2025 is a maximum of $6,032, according to the CRA’s indexation chart.

- The provincial DTC portion is approximately 10% (the percentage varies from province to province) of the disability amount for that tax year.

What is the Disability Tax Credit Base Amount for 2026

If the eligible person is an adult, he or she will only receive the federal and provincial Disability Tax Credit (DTC) “Base Amount”. The provincial percentage ranges by province.

For example (using Ontario 2025 figures):

- The federal disability base amount for 2025 is $10,341, and 14.5% of that is $1,499.45

- The provincial disability base amount in Ontario for 2025 is $10,341, and 5.05% of that is $522.22

- Therefore in 2026, a DTC-eligible adult in Ontario would have received for Tax year (2024-2025): $1,499.45 + $522.22 = $2,021.67

What is the Disability Tax Credit Supplemental Amount for 2026

If the eligible person is under 18 years of age at the end of the tax year, then he or she will be eligible to receive the Disability Tax Credit (DTC) “Base Amount” as well as the DTC “Supplemental Amount.” The provincial percentage ranges by province.

For example (using Ontario figures):

- The federal supplemental disability amount for 2025 is $6,032, and 14.5% of that is $874.64

- The provincial supplemental disability amount for 2025 is $6,032, and 5.05% of that is $304.62

Therefore, a DTC-eligible minor in Ontario would have received:

- “Base Amount” as calculated above of $2,021.67

- “Supplemental Amount” of $874.64 + $304.62 = $1,179.26

If we add the “Base Amount” and “Supplemental Amount,” we will see that an eligible person under 18 years of age in Ontario would receive $3,200.93 in Disability Tax Credits for the 2025 tax year.

To make it easier to understand and calculate the approximate disability tax credits you are eligible for, you can follow the formula below:

- An eligible adult can receive a total of $1,800–$2,300 per year of eligibility.

- An eligible minor can receive a total of $3,000–$4,000 per year of eligibility.

NOTE: To summarize, to calculate the total amount of DTC you are eligible to receive, you need to multiply the number of years by the amount per year.

Calculating Your 10-Year Retroactive Disability Tax Credit Payment

Important Note: Retroactive Amounts

The retroactive amounts shown below are general estimates only. Actual tax reductions depend on several factors, including the number of years approved, income tax payable in those years, province or territory of residence, and whether the credit is claimed directly or transferred to a supporting person. DTC approval does not guarantee a refund, and amounts will vary based on individual tax circumstances.

Calculating your 10-year retroactive refund is more or less the same as calculating for your current year. The only difference is that you will be using the maximum Disability Amounts of the Year to get the retroactive payment. Below is a chart that details these amounts. As a rough estimate, however, you may receive up to the following:

- If an adult is found eligible to receive the DTC for the past 10 years, he/she will receive between $15,000 and $25,000 in a lump sum amount.

- If a minor is found eligible to receive the DTC for the past 10 years, he/she will receive between $30,000 and $45,000 in a lump sum amount.

If your DTC application has been approved and you are trying to figure out how much you’ll be receiving, our Disability Tax Credit Calculator is available here to further understand and estimate your refunds.

Estimate Your Potential DTC Amount

If you would like a rough estimate based on your province and years of eligibility, you can use our Disability Tax Credit calculator. This tool provides an approximate projection for informational purposes only and does not guarantee approval, refund amounts, or retroactive payment. Actual results depend on CRA approval and your individual tax circumstances.

Maximum Federal Disability Amounts by Year (Including Maximum Child Supplement)

The chart below shows CRA’s indexed maximum federal Disability Tax Credit amounts by tax year, including the maximum supplement for individuals under 18.

| Tax Year | Maximum Disability Amount | Maximum Supplement (Under 18) |

| 2025 | $10,341 | $6,032 |

| 2024 | $10,138 | $5,914 |

| 2023 | $9,872 | $5,758 |

| 2022 | $9,428 | $5,500 |

| 2021 | $8,870 | $5,174 |

| 2020 | $8,662 | $5,053 |

| 2019 | $8,576 | $5,003 |

| 2018 | $8,416 | $4,909 |

| 2017 | $8,235 | $4,804 |

| 2016 | $8,113 | $4,733 |

| 2015 | $8,001 | $4,667 |

| 2014 | $7,899 | $4,607 |

| 2013 | $7,766 | $4,530 |

| 2012 | $7,546 | $4,402 |

| 2011 | $7,341 | $4,282 |

| 2010 | $7,239 | $4,223 |

| 2009 | $7,196 | $4,198 |

How Does the Disability Tax Credit Affect Your Other Governmental or Provincial Benefits?

DTC approval does not automatically change most other federal, provincial, or territorial benefits, since each program has its own rules.

In most cases, the DTC will not reduce or cancel supports such as provincial disability assistance, student funding, housing programs, or employment benefits. However, DTC approval may help you qualify for other disability-related programs and savings supports that require CRA confirmation.

Because eligibility varies by program and province, it is important to confirm details with each administering authority.

Once You’re Approved for Disability Tax Credit, you are eligible for several other federal, provincial, or territorial programs, such as:

The Registered Disability Savings Plan (RDSP)

The Registered Disability Savings Plan (RDSP) is a long-term savings plan available to eligible Canadians with disabilities. Approval for the Disability Tax Credit may allow an individual to open an RDSP.

The plan allows contributions to grow tax-deferred and may include federal disability savings grants and bonds, depending on income and other criteria. Contributions can be made by the beneficiary or others on their behalf.

RDSPs are designed for long-term financial security and are subject to specific rules around contributions, withdrawals, and eligibility.

Canada Disability Benefit (CDB)

The Canada Disability Benefit (CDB) is a new federal income support program for working-age Canadians with disabilities who are approved for the Disability Tax Credit. Beginning in July 2025, the federal government intends to provide up to $2,400 per year to eligible low-income individuals to help improve financial stability and reduce poverty.

The CDB is designed to work alongside existing provincial and territorial programs rather than replace them. Eligibility depends on DTC approval, along with income and other criteria set out in federal regulations.

Budget 2025 also proposes a $150 supplemental payment to help offset the cost of obtaining DTC certification or re-certification when it results in CDB entitlement. These payments are expected to be issued retroactively to the launch of the benefit, with implementation anticipated by 2026–27 following regulatory updates.

Child Disability Benefit

The Child Disability Benefit is a tax-free monthly payment for families caring for a child under 18 who has been approved for the Disability Tax Credit. Payment amounts depend on the number of eligible children and the family’s adjusted net income.

CRA recalculates Child Disability Benefit payments every July using the adjusted family net income from the previous year’s tax return. For example, payments from July 2025 to June 2026 are based on income reported on the 2024 tax return.

For the July 2025 to June 2026 benefit period, families may receive up to $3,411 per eligible child per year (up to $284.25 per month). The benefit begins to reduce once adjusted family net income exceeds $81,222. The reduction rate differs depending on whether one child or multiple children qualify.

Canada Workers Benefit – Disability Supplement

The Canada Workers Benefit Disability Supplement provides additional financial support to low-income workers with disabilities. Individuals who qualify for the Disability Tax Credit and meet income requirements may be eligible for this supplement.

The amount received depends on earnings, marital status, and other CRA criteria, and is claimed through the annual tax return.

Canada Caregiver Credit

The Canada Caregiver Credit is a non-refundable tax credit available to individuals who provide support to a spouse, common-law partner, child, or other dependent with a physical or mental impairment. Eligibility depends on the relationship, the dependent’s net income, and the level of support provided during the year.

For children under 18 at the end of the tax year, you may be able to claim $2,687 per eligible child on line 30500 of your income tax return, subject to CRA rules and income thresholds.

For dependents aged 18 or older who are not your spouse or common-law partner, you may be able to claim up to $8,601 per eligible dependent on line 30450. This applies to certain adult dependents who are not already claimed as an eligible dependent on line 30300 or 30400.

In many cases, approval for the Disability Tax Credit can support eligibility for the Canada Caregiver Credit, although each credit is assessed separately under CRA guidelines.

Canada Disability Savings Grant and Bond

The Canada Disability Savings Grant and Canada Disability Savings Bond are federal contributions available through the Registered Disability Savings Plan.

The Canada Disability Savings Bond may provide up to $1,000 per year to eligible low- and modest-income families, even when no personal contributions are made.

The Canada Disability Savings Grant may provide matching contributions when funds are added to an RDSP. Depending on contribution amounts and income thresholds, the government may contribute up to $3,500 per year.

Both programs are subject to lifetime limits and income-based eligibility rules.

Home Accessibility Tax Credit

The Home Accessibility Tax Credit is a non-refundable tax credit for qualifying renovation expenses that improve accessibility or safety for a person with a disability or a senior. Eligible expenses may include modifications such as ramps, walk-in showers, or other barrier-reducing improvements.

Proposed changes would increase the annual expense limit to $20,000, potentially allowing a federal tax credit of up to $3,000, depending on the applicable tax rate.

Disability Tax Credit Case Studies

The following case summaries illustrate how Disability Tax Credit applications can succeed when eligibility criteria are clearly documented and functional limitations are properly explained. Each example reflects a different impairment category and outcome following CRA review.

Sadie, age 5, Ontario — Ehlers-Danlos Syndrome

Sadie was diagnosed with Ehlers-Danlos Syndrome at age three. She requires constant supervision to perform daily activities and uses a Spio suit to support joint stability. Ongoing speech therapy and physiotherapy are also part of her care.

Her initial DTC application was denied. After reviewing the original submission, clarifying functional limitations, and working with her medical providers, a revised application was submitted. CRA approved eligibility for the 2021 to 2025 tax years.

Estimated outcome:

Approximately $15,000–$17,000 in retroactive Disability Tax Credit–related tax reductions and benefit adjustments, with continued eligibility for child-related disability benefits going forward.

Greg, age 65, Ontario — Osteoarthritis

Greg was diagnosed with osteoarthritis in 2021 and underwent knee surgery due to extensive joint damage. He takes significantly longer to walk, dress, and move between positions, and experiences persistent pain that limits daily functioning.

CRA approved Greg’s DTC application based on marked restrictions in mobility and self-care. Eligibility was granted for the 2021 to 2024 tax years.

Estimated outcome:

Approximately $8,000–$9,000 in retroactive tax reductions.

Louis, age 58, Quebec — Type 1 Diabetes

Louis manages Type 1 diabetes through multiple daily insulin injections and frequent blood glucose monitoring. His treatment routine requires consistent daily time that meets CRA’s life-sustaining therapy criteria.

After documenting therapy time and medical necessity, CRA approved his application for the 2021 to 2024 tax years.

Estimated outcome:

Approximately $8,000–$9,000 in retroactive Disability Tax Credit–related tax reductions.

Ruta, age 55, Ontario — Major Depressive Disorder

Ruta has lived with a severe depressive disorder for decades. Her condition significantly affects judgment, decision-making, and the ability to manage daily activities independently. CRA initially requested additional clarification from her physician.

After further medical documentation was provided, CRA approved her eligibility for the 2021 to 2024 tax years.

Estimated outcome:

Approximately $8,000–$9,000 in retroactive tax reductions.

J’yquan, age 18, Ontario — ADHD and Learning Disability

J’yquan was diagnosed in early childhood with a learning disability and ADHD. His impairments affect memory, judgment, personal care, and daily functioning. His case required detailed functional documentation and coordination with family and medical providers.

CRA approved eligibility from 2018 through 2024.

Estimated outcome:

Approximately $20,000–$22,000 in combined retroactive tax reductions and child-related disability benefit adjustments.

Important Note: Amounts shown above are estimates based on indexed Disability Tax Credit values, applicable tax rates, and approved eligibility periods. Actual results vary depending on income tax payable, province of residence, and whether credits were claimed directly or transferred to a supporting person.

How the Disability Tax Credit Program Developed

Canada’s Disability Tax Credit originally applied to a narrow group of impairments, with limited recognition before the mid-1980s. Over time, as disability data improved and eligibility standards evolved, CRA expanded the categories and refined how functional limitations are assessed.

A major shift occurred in 2005, when eligibility became centered on whether an impairment is severe and prolonged, focusing on long-term functional impact rather than diagnosis alone. This framework continues to guide CRA decisions today.

Conclusion

The Disability Tax Credit exists to help reduce income tax for Canadians living with disabilities. It is not limited to individuals with the most severe conditions. Many people who experience ongoing difficulty with everyday activities may qualify, even if they are still able to work.

The DTC has provided meaningful tax relief to hundreds of thousands of Canadians. Still, many eligible individuals remain unaware of the criteria or underestimate how important clear and complete medical documentation can be. Submitting Form T2201 alone does not guarantee approval. The strength of the application depends on how well functional limitations are explained and supported.

This guide was created to help you understand the process and approach the DTC application with greater confidence. If you need assistance, our team offers expert services on a no-win, no-fee basis. You can begin with a free assessment to better understand your options.

At Disability Credit Canada, we are proud to support Canadians seeking access to the Disability Tax Credit, CPP-Disability, and long-term disability benefits.